Source: TRT World

Business

Indian rupee hits new record low, breaches 80 per dollar

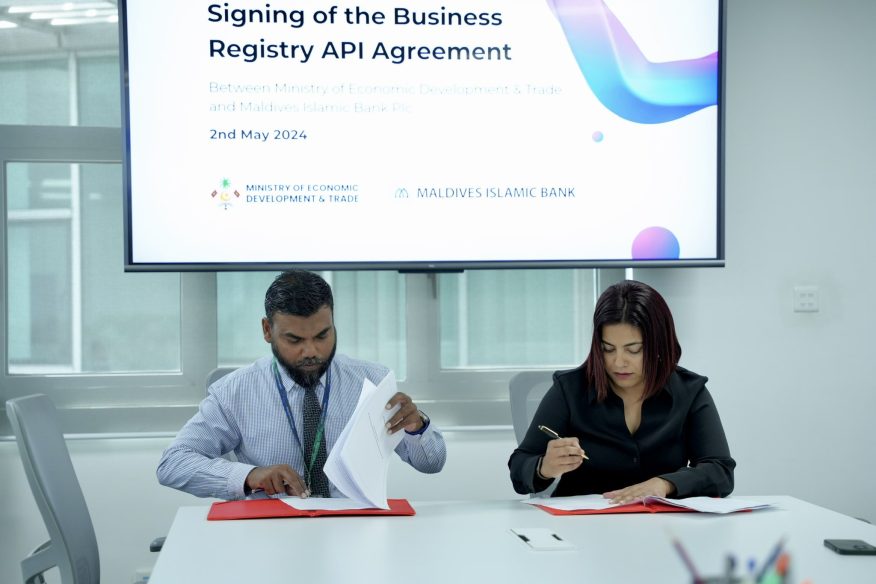

Ministry of Economic Development and Trade and the Maldives Islamic Bank (MIB) has entered an agreement, aiming to expedite and streamline the registering services for businesses. The agreement was signed to enhance the quality of services, ensure information security, and facilitate an efficient registration process.

Following the signing of the agreement, Minister of Economic Development and Trade Mohamed Saeed disclosed that customer data can be readily verified with the assistance of the ministry’s Application Programming Interface (API). The minister stated that this would enable businesses to set up bank accounts in a convenient manner. Regarding this, Registrar of Companies Mariyam Waheed underscored the pivotal role API will play in authenticating businesses to customers and expediting in the verification process.

This initiative will significantly benefit individuals accessing online services from the ministry, fostering economic development within the nation. This marks the first agreement of its kind signed by the ministry.

Business23 hours ago

MIB signs an agreement to expedite business registration process

News23 hours ago

Freedom of journalism must be practiced within the responsibilities

News1 day ago

Fourth meeting of High-Level Core Group on withdrawal of Indian troops held in Delhi

Tech1 day ago

Google trial wraps up as judge weighs landmark U.S. antitrust claims

News2 days ago

Minister of Islamic Affairs to attend the OIC Summit as the President’s Special Envoy

Sports2 days ago

Preview: Title, Europe, relegation intertwined in dramatic Premier League weekend

News2 days ago

Vice President pledges govt’ support for journalists welfare

News3 years ago

Elections Commission grants approval to form Maldives Solidarity Party.

Local3 years ago

Parliament’s 06th May Terror Attack Report Highlights Defence Minister Mariya Ali Didi’s Negligence.

Local3 years ago

Former President Mohamed Nasheed revokes support for the current administration in an open letter.

Local3 years ago

Leaked documents show India refused to withdraw military personnel and helicopters from the Maldives even after their Visa’s expired.

Opinion3 years ago

Hiyaa flats- pigeon coops, negative stereotyping and lobbying.

Local2 years ago

President Abdulla Yameen officially calls for the removal of Indian military personnel in the Maldives.

Local2 years ago

Contact with 20 Maldivian student pilots stranded in Philippines lost as super typhoon Rai slams the nation.

-

News7 days ago

News7 days agoEfforts underway to submit new laws to Parliament

-

News5 days ago

News5 days agoMinister states only 1% of 8% plastic waste is recycled

-

Sports5 days ago

Sports5 days agoAhead of Paris duel: Sancho on bumpy road to his top level

-

News7 days ago

News7 days agoFushidhiggaru project ongoing, will finish on time: Government

-

News5 days ago

News5 days agoUnauthorised domain holders to be offered legal compliance

-

Sports5 days ago

Sports5 days agoAsian Carrom Championship: silver for men, bronze for women

-

World4 days ago

World4 days agoUN chief calls for Israel-Hamas accord, int’l probe of mass graves in Gaza

-

News4 days ago

News4 days agoGovernmenr condemns threats against media; vows to protect journalists