Business

Issues Facing Institutions offering Takaful in Maldives.

Takaful is the first type of Islamic financial service provided in Maldives. In 2003, Amana Takaful Maldives began as an agency operation offering takaful services and later it began as an incorporated company established for the purpose by obtaining a conventional insurance license from Maldives Monetary Authority (MMA). Though it has been 18 years since then, still Amana Takaful Maldives is operating under the same conventional insurance license given to them and there is no separate framework applicable to them. Apart from Amana Takaful Maldives, Ayady Takaful which is the Islamic window of Allied Insurance Maldives offers takaful services since 2014. In terms of takaful products, Amana Takaful Maldives offers general takaful products while Ayady takaful provides both general and family takaful products.

What is Takaful?

Takaful is also known as Islamic insurance. The term takaful is derived from the Arabic word “Kafalah” which means responsibility or guarantee. Takaful is derived from the Muslim historic system of ‘aqilah where the blood money that needs to be paid by the murderer to the family of the deceased with be jointly paid by the family of the murderer. Researchers such as ISRA (2011)[1] has divided the developments of takaful into four phases where: phase one is in 1979 when the first takaful model based on ta’awuni model (cooperative) was developed in Sudan; phase two is in 1984 when mudharabah model was developed in Malaysia; phase three is in the same year where wakalah model was developed in gulf for takaful; and the final phase is in 1996 when waqf model was developed in South Africa. In takaful, takaful operator is not the insurer insuring the participants and it is the persons participating in the scheme who are known as takaful participants that mutually insure one another by mutually guaranteeing each other. As such, the role of takaful operator is to act as administrator of the takaful fund whose responsibility includes managing and investing the fund according to the shariah principles. The main differences between takaful and conventional insurance are provided below.

Source: ISRA (2011)

Issues facing Takaful Institutions in Maldives

There are number of issues facing the growth of takaful industry in Maldives. Below explained are the most critical issues faced in this regard.

- Lack of separate legal framework to govern Takaful: At the moment in Maldives, the same rules applicable to conventional insurance is applied to takaful. There are no separate legal requirements for takaful making takaful service offering institutions to have no difference in this regard with the existing conventional insurance players in the market. It is stated in the official website of MMA that insurance industry is regulated by MMA under the powers provided in the MMA Act 1981 and it is the Insurance Industry Regulation (2004) and insurance guidelines that set out specific criteria for authorization and other regulatory requirements to undertake business as insurers and insurance intermediaries in the Maldives. Article 1 of the Insurance Industry Regulation (2004) also states that in accordance with the provisions of the Presidential Decree no 2002/6 dated 16th January 2002, MMA as the designated competent authority has sole responsibility for the regulation and supervision of the insurance industry in the Republic of the Maldives. Since takaful is different from conventional insurance, the modus operandi of takaful need to be regulated within the parameters of Shariah rules applicable to it and regulatory clear guidance in the operational aspects of takaful offering institutions are essential to ensure that there is no breach of Shariah rules in offering of the service while safeguarding the rights of the customers and other stakeholders.

- Lack of Shariah governance standards for Takaful: Adoption of Shariah governance standards are important to achieve shariah compliance. The Shariah internal control functions that ought to be implemented within a takaful service offering institution need to be crystalized and standardized uniformly by the regulatory authority as without these internal control functions, managing Shariah non-compliance risk within the takaful service offering institutions will be a challenge. Likewise, there is also need for the regulatory authority to establish adequate mechanisms to report and disclose Shariah non-compliance events happening within the takaful service offering institutions.

- Lack of Short-term Shariah compliant investment avenues: Unlike conventional insurance companies, takaful service offering institutions cannot participate in the interest-based investment activities. Since there are limited Shariah compliant investment opportunities in Maldives, there is need to find ways to provide diversified investment opportunities for the takaful offering institutions to invest their funds. In this regard, it is imperative to introduce a well-regulated Islamic money market in the country where short-term liquidity management opportunities could be made available to all Islamic financial institutions.

- Absence of opportunity for Amana Takaful Maldives to place mandatory deposit kept with MMA in a Shariah compliant way: At the moment, there is no mechanism to keep mandatory deposits of Amana Takaful Maldives in a shariah compliant manner which has resulted in the company being unable to use the return received as the return received in this regard is considered as “tainted income” that needs purification. According to Guideline on Prudential Requirements for Insurance Undertakings 2010, all authorized insurance undertaking, whether life or general insurance shall at all times maintain a deposit of MVR 2 million with MMA, for each type of insurance (life or general insurance) the undertaking is authorized to engage in and all deposits placed with MMA for this purpose will be remunerated. Therefore, it is important for MMA to ensure that there is a Shariah compliant mechanism to place this deposit for takaful offering institutions to ensure that the return from these deposits could be used by the takaful offering institutions. In the Annual Report of Amana Takaful Maldives of 2020, following statement is found in the report of the Shariah Advisory Council the company:

An amount of money credited to the Waqf fund from mandatory interest based placement with the MMA has been designated to be paid to charity. Management has been advised to continue to canvass the MMA to convert this placement to a Shariah Compliant placement

Conclusion

There is no doubt that takaful industry has seen exponential development over the years in Maldives. However, to take the local takaful industry to the next level, there is need to eliminate the issues facing the takaful institutions operating in the country. The most important action in this regard is to introduce a distinct takaful legal and governance framework to the country. By doing so, a favorable environment for the existing market players will be created while attracting new players to the industry.

Dr. Aishath Muneeza is an Associate Professor at the International Center for Education in Islamic Finance.

[1] International Shari’ah Research Academy for Islamic Finance (ISRA), (2011). ‘Islamic Financial System Principles & Operations’, (Kuala Lumpur, ISRA; Malaysia).

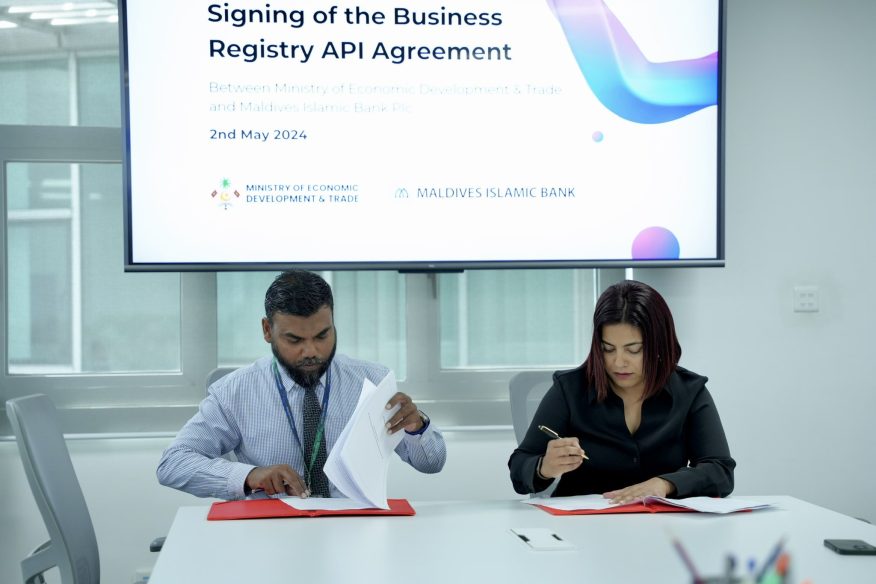

Ministry of Economic Development and Trade and the Maldives Islamic Bank (MIB) has entered an agreement, aiming to expedite and streamline the registering services for businesses. The agreement was signed to enhance the quality of services, ensure information security, and facilitate an efficient registration process.

Following the signing of the agreement, Minister of Economic Development and Trade Mohamed Saeed disclosed that customer data can be readily verified with the assistance of the ministry’s Application Programming Interface (API). The minister stated that this would enable businesses to set up bank accounts in a convenient manner. Regarding this, Registrar of Companies Mariyam Waheed underscored the pivotal role API will play in authenticating businesses to customers and expediting in the verification process.

This initiative will significantly benefit individuals accessing online services from the ministry, fostering economic development within the nation. This marks the first agreement of its kind signed by the ministry.

Maldivians must always advocate for rights of Palestinians: Minister Haidar

BML announce new MVR 1-mil loan facility without collateral

Maldives sweeps WTAs with four titles in Indian Ocean category

Gaza truce uncertain, Hamas to deliver ‘final response’ in two days

MWSC contracted to upgrade Addu City’s water view

MIB signs an agreement to expedite business registration process

Freedom of journalism must be practiced within the responsibilities

Elections Commission grants approval to form Maldives Solidarity Party.

Parliament’s 06th May Terror Attack Report Highlights Defence Minister Mariya Ali Didi’s Negligence.

Former President Mohamed Nasheed revokes support for the current administration in an open letter.

Leaked documents show India refused to withdraw military personnel and helicopters from the Maldives even after their Visa’s expired.

Hiyaa flats- pigeon coops, negative stereotyping and lobbying.

President Abdulla Yameen officially calls for the removal of Indian military personnel in the Maldives.

Contact with 20 Maldivian student pilots stranded in Philippines lost as super typhoon Rai slams the nation.

-

News6 days ago

News6 days agoMinister states only 1% of 8% plastic waste is recycled

-

Sports6 days ago

Sports6 days agoAhead of Paris duel: Sancho on bumpy road to his top level

-

News6 days ago

News6 days agoUnauthorised domain holders to be offered legal compliance

-

World6 days ago

World6 days agoUN chief calls for Israel-Hamas accord, int’l probe of mass graves in Gaza

-

Sports6 days ago

Sports6 days agoAsian Carrom Championship: silver for men, bronze for women

-

News6 days ago

News6 days agoGovernmenr condemns threats against media; vows to protect journalists

-

News5 days ago

News5 days agoPresident: Solely increasing salaries not a solution, employees require education and training

-

News6 days ago

News6 days agoInvestor confidence boosted with election win: Minister Saeed